KILLER ANGELS

July 10, 2018

Bill Hackney, CFA

Atlanta Capital

404-876-9411

bill.hackney@atlcap.com

In July 1863, the American Civil War reached a decisive turning point in the gently rolling hills of southeastern Pennsylvania. Until the Battle of Gettysburg, Confederate armies frustrated President Lincoln with an unsettling string of victories. After Gettysburg, the tide began to change in favor of the Union.

Perhaps the best known book about Gettysburg is the historical novel The Killer Angels by Michael Shaara. It won a Pulitzer Prize, was the inspiration for Ken Burns’ popular TV documentary series, The Civil War, and is required reading at most Army and Marine Corps officer schools. The book is essentially a character study of the key protagonists on both sides of the conflict. Its title, taken from a speech by Union Colonel Joshua Chamberlain, is a metaphor for the duality of man’s nature, i.e., his innate capacity for both good and evil, both righteousness and destruction.

So how does Shaara’s opus and the Battle of Gettysburg relate to today’s investment climate? One key protagonist that has always shaped the outlook for the stock and bond markets is inflation. It too has a dual nature, with the capacity to inflict both good and evil. For more than three decades, inflation has generally trended lower, inflicting more pleasure than pain on the capital markets. While inflation in the US is unlikely to surge in the near term, it has reached a decisive turning point in my view. The best of the inflation news is likely behind us.

Why the dual nature of inflation? Two key goals of our Federal Reserve are to promote price stability and maximum employment. Price instability fouls up the credit markets and thereby reduces the ability of an economy to grow. High inflation makes lenders reluctant to lend. Deflation (falling prices) undermines the value of collateral and makes borrowers reluctant to borrow. What’s more, rising inflation in goods and services tends to depress stock and bond prices. In fact, hyperinflation can destroy governments and economies: think Germany’s Weimar Republic in the 1920s or Venezuela today.

Price stability or a small amount of inflation is essential to the health of both the economy and the capital markets. For much of the past nine years, the Fed has focused on creating sufficient inflation to push it up to its 2% target. In the past few months, it is clear that the goal has now been achieved—all key measures of consumer price inflation are showing inflation at 2% or more.

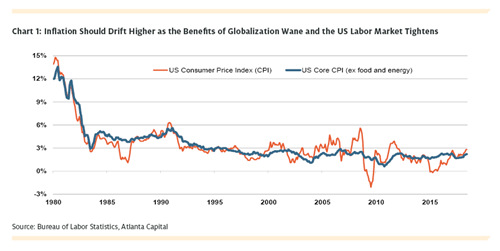

Chart 1 shows monthly data for the headline Consumer Price Index (all items) and the core CPI (excluding food and energy) from 1980 - May 2018. The most recent readings were 2.8% and 2.2%, respectively.

The Fed generally pays more attention to core inflation than the headline number. There are two reasons for this: 1) the trend in the core number is much less volatile and therefore better for policy setting purposes, and 2) most Fed governors believe that it would be inappropriate to tighten monetary policy (raise interest rates) due to an inflation spike caused solely by higher commodity prices. (Commodity prices are often influenced by geopolitical forces beyond the Fed’s control and higher commodity prices often reduce consumer spending in other areas of the economy.)

Core CPI is likely to drift steadily higher over the next 12-18 months, possibly hitting 3% by the end of 2019. This should keep steady upward pressure on interest rates and downward pressure on bond prices. While stocks are better positioned to deal with inflation, price/earnings ratios will be under pressure from rising interest rates, which should limit stock price appreciation in 2019 and beyond.

I will be the first to admit that predicting the US inflation rate more than a few quarters ahead has been a fool’s errand for much of this nine-year old economic cycle. Most prognosticators, including yours truly, predicted that more of the Fed’s massive monetary stimulus would have found its way into the prices of goods and services. But that hasn’t happened. Not yet at least.

Global Benefits Are Waning

So why could inflation make a decisive turn now? It’s a combination of secular, cyclical and political factors, which in my view are sufficiently potent to trigger a reversal in the 35-year downtrend in inflation.

One of the principal reasons that inflation has declined since the early 1990s is globalization—the increased integration of world economies through free trade, the free flow of capital and people, and the tapping of cheaper labor markets by multinational companies. Globalization unleashed massive deflationary forces on the world economy. The unraveling of the USSR in late 1989 brought a flow of cheap labor from eastern Europe into more productive, capitalist-oriented countries. The North American Free Trade Agreement (NAFTA) went into effect in 1994, reducing trade barriers among the US, Mexico and Canada and sparking an intricate web of cross-border supply chains to cut costs. In 2001, China joined the World Trade Organization. International trade with China exploded as many western companies and consumers took advantage of low cost Chinese labor.

The deflationary benefits of globalization have largely played out in my opinion. There are two reasons: one demographic and one political. Demographically, the work force of Europe stopped growing around 2010 and the work force of China stopped growing around 2016. Given their low birth rates and policies toward immigration, both regions are likely to experience no labor force growth for several decades. In short, the vast reservoirs of cheap labor which drove disinflation over the past three decades are gone. What’s more, absent immigration, the US is unlikely to experience much labor force growth either. Maybe India and Africa can take up the slack, but I doubt it.

Politically, globalization doesn’t seem to have much popular support these days. There’s Brexit—the UK planning to leave the European Union. There’s the rise of anti-immigrant political parties throughout Europe. During the 2016 US presidential election, both parties shot down the Trans-Pacific Partnership Agreement. NAFTA is now being renegotiated. The Trump Administration has implemented a number of tariffs on goods from China as well as many other nations. Most nations, of course, retaliated. Tariffs are a tax which raises costs to consumers. Uncertainty over tariffs and trade agreements make it difficult for companies to control costs or make wise capital investment decisions.

Beyond the waning benefits of globalization are the cyclical pressures on inflation from a tightening labor market in the US. In past economic cycles, when the unemployment rate reached about 4% or lower, annual wage inflation began to rise sharply, often hitting 4% or higher. This often prompted the Fed to hike interest rates more aggressively because wages and salaries make up a major component of the cost of goods and services.

Wage Inflation Restrained for Now, However...

During the current cycle, wage gains have been more restrained. In June’s Employment Situation Report, released on July 6th, the unemployment rate actually ticked up from 3.8% to 4.0% and the annual gain in average hourly earnings was a modest 2.7%. This news was received by both the stock and bond markets as a favorable sign—despite entering its tenth year, the aging US economic expansion has yet to show troublesome signs of wage inflation. However, with more and more companies reporting labor shortages and business optimism running high, I think that it’s just a matter of time before wage gains accelerate to 3.5% or more.

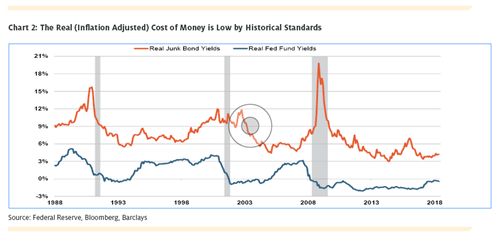

There is more risk to the bond market, however, than just rising inflation. Chart 2 shows trends in real interest rates over the past 30 years. To calculate the real cost of money, I subtract the prevailing inflation rate from the interest rate. Note that since the Great Recession of 2008-2009 the real fed funds rate has been negative, indicating a super easy monetary policy. For the less-than-investment-grade borrower, the real cost of money is about 4.2% currently, with a range of between 3% and 9% since the recession.

The 30-year average for the real fed funds rate is 0.8% or 80 basis points. This would imply a fed funds rate of 3% given the current core inflation rate of 2.2%. However, the current fed funds rate is only 1.9%. For junk bonds the 30-year average real rate is 7.5% versus a current real rate of only 4.2%. Granted, real interest rates do jump around a lot, but it is unusual for real interest rates to be trading this far below their historical averages during the mature phase of an economic expansion. The point is that real interest rates seem unusually low, so current nominal interest rates don’t provide investors much of a premium over inflation.

More Borrowing by Government and Business

But wait! There’s more! As the TV pitchman might say. Besides inflation creeping up and real interest rates seeming too low, the demand for credit in our economy appears to be getting overheated. Thanks to the recent tax cuts, federal government tax receipts dropped almost 5% during the first quarter. Coupled with increased government spending, government borrowing leaped a whopping 15% during the first quarter. One study estimates that the US will borrow the equivalent of 25% of its GDP this year to finance its deficit and refinance maturing debt. Not the kind of government borrowing you expect to see in a strong economy with low unemployment.

At this rate, it’s just a matter of time before the feds begin “crowding out” the private sector from the credit markets. But maybe it’s just as well. The US corporate sector is already loaded up with debt, much of it to finance acquisitions and share repurchases. Corporate debt as a percent of GDP has recently ramped up to levels last seen at the peaks of the two previous economic cycles. Commercial and Industrial loan demand at banks, which slumped during 2016-2017, has strengthened this year along with small business expansion plans. Much of the corporate debt accumulated during the current economic cycle has been of lesser quality than that accumulated during prior cycles. Covenant-lite loans, leveraged loans, and junks bonds all have gained share of overall corporate lending.

Too Much Complacency in Bonds

Given all of the above, I think the US bond market has been remarkably calm this year, eerily calm you might say. After an initial pop in rates in January, the 10-year Treasury yield has traded between 2.8 and 3.1% and closed the quarter at 2.85%. Credit spreads—the gap between lower quality bond yields and Treasuries—have widened a bit recently, but remain narrow, reflecting too much complacency among investors who still appear to be chasing yield and ignoring risk. With higher inflation on the way and credit spreads more likely to widen than tighten, fixed income investors should emphasize higher quality, shorter maturities.

Investors with an appetite for risk should still look to the stock market. Using the S&P 500® index current price of 2670, the stock market trades at 17.2 times estimated earnings of $160, with a dividend yield of 1.8%. This valuation is not dirt cheap, but not unreasonably high given a 3% inflation rate and prospective growth in earnings and dividends of about 5% in 2019.

Eventually the Killer Angels of inflation and the credit markets will turn against the US economy and stock market. But first they must turn against the bond market. That hasn’t happened yet, but I can hear them flapping their wings.

This material is presented for informational and illustrative purposes only and should not be construed as investment advice, a recommendation to purchase or sell specific securities, or to adopt any particular investment strategy. The opinions expressed herein are those of the author and do not necessarily reflect the views of other employees at Atlanta Capital Management. Any current investment views and opinions/analyses expressed constitute judgments as of the date of this material and are subject to change at any time without notice. Index and commodity changes are based on price-only percentage change. This material has been prepared on the basis of publicly available information, internally developed data, and other third party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and Atlanta Capital has not sought to independently verify information taken from public and third party sources. This material may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions. Investing entails risks and there can be no assurance that any forecasts or opinions expressed in this material will be realized. It is not possible to directly invest in an index. Past performance does not predict future results.